What FOMC Black Sheet Means for Inflation, GDP and Rate Cuts

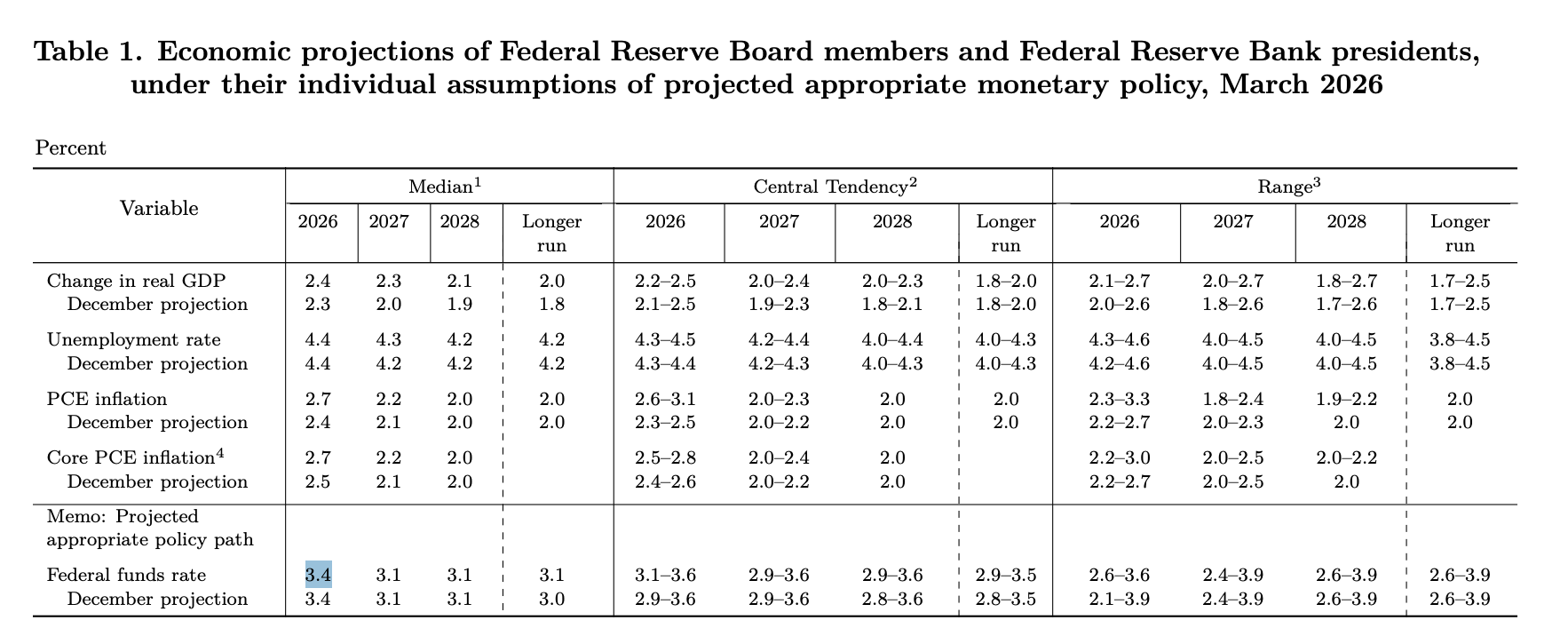

On March 18, 2026, the Federal Open Market Committee (FOMC) released its latest Summary of Economic Projections (SEP), following the March 17–18 policy meeting. This document reflects the individual forecasts of the 19 FOMC participants for real GDP growth, the unemployment rate, headline and core PCE inflation, and the appropriate path for the federal funds rate through 2028 and the longer run.

Compared with the December 2025 projections, the March update shows modestly stronger expected GDP growth and noticeably higher near-term inflation, while the median interest-rate path remains unchanged in the near term and edges only slightly higher over the longer run.

Below is a general overview of the key changes across the main variables.

Real GDP Growth: Modest Upgrade Across the Horizon

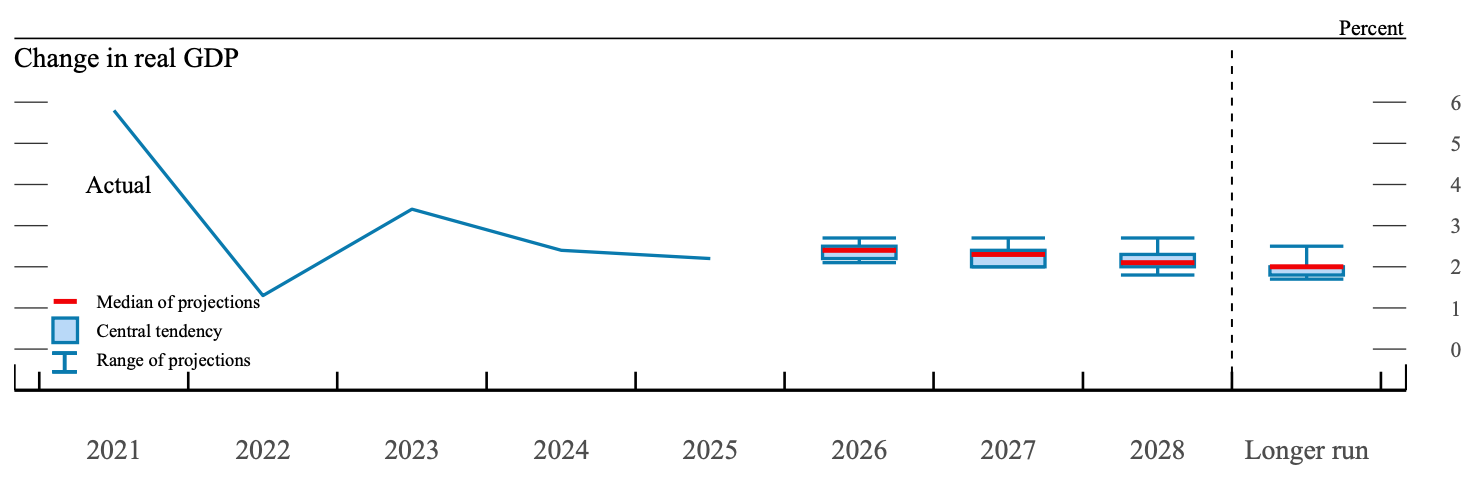

The median projection for real GDP growth (Q4-over-Q4) was revised upward to 2.4% for 2026 (from 2.3% in December), 2.3% for 2027 (from 2.0%), and 2.1% for 2028 (from 1.9%). The longer-run median also rose to 2.0% (from 1.8%).

| Year | March 2026 Median | December 2025 Median | Change |

|---|---|---|---|

| 2026 | 2.4% | 2.3% | +0.1 pp |

| 2027 | 2.3% | 2.0% | +0.3 pp |

| 2028 | 2.1% | 1.9% | +0.2 pp |

| Longer run | 2.0% | 1.8% | +0.2 pp |

Table 1. FOMC median GDP forecast in March 2026 vs December 2025.

Central tendency ranges shifted higher as well. Overall, the Fed now anticipates the economy will run with somewhat more momentum over the next few years than it expected three months ago, while still converging toward its estimated longer-run trend of around 2%.

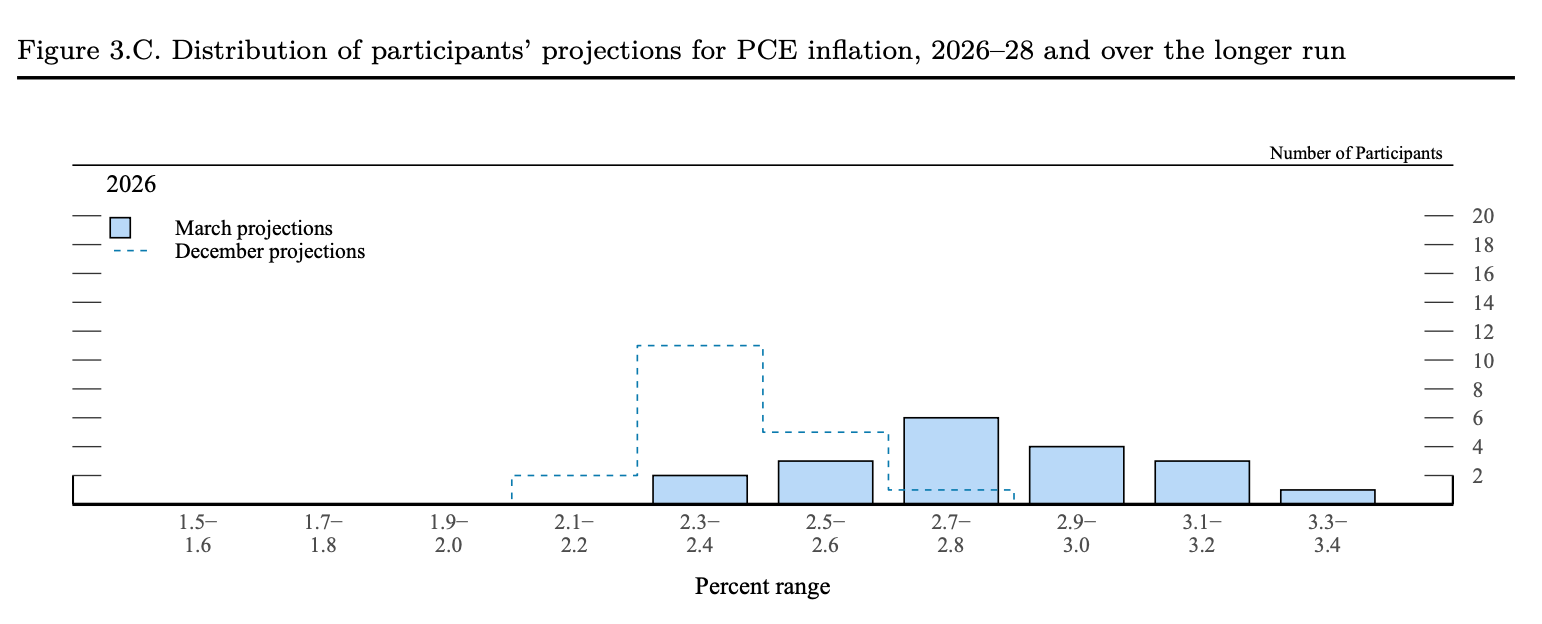

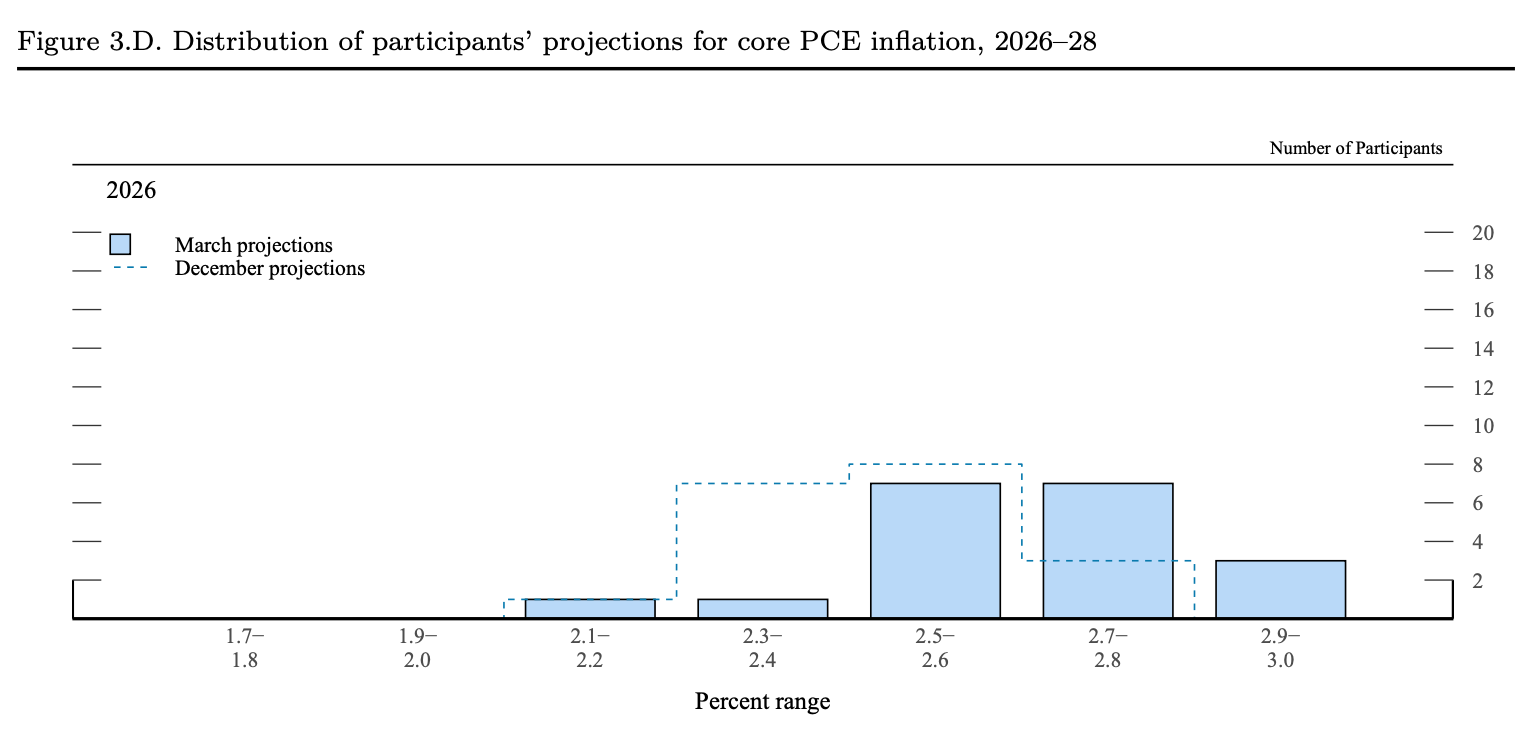

PCE Inflation: Notable Near-Term Revisions Higher

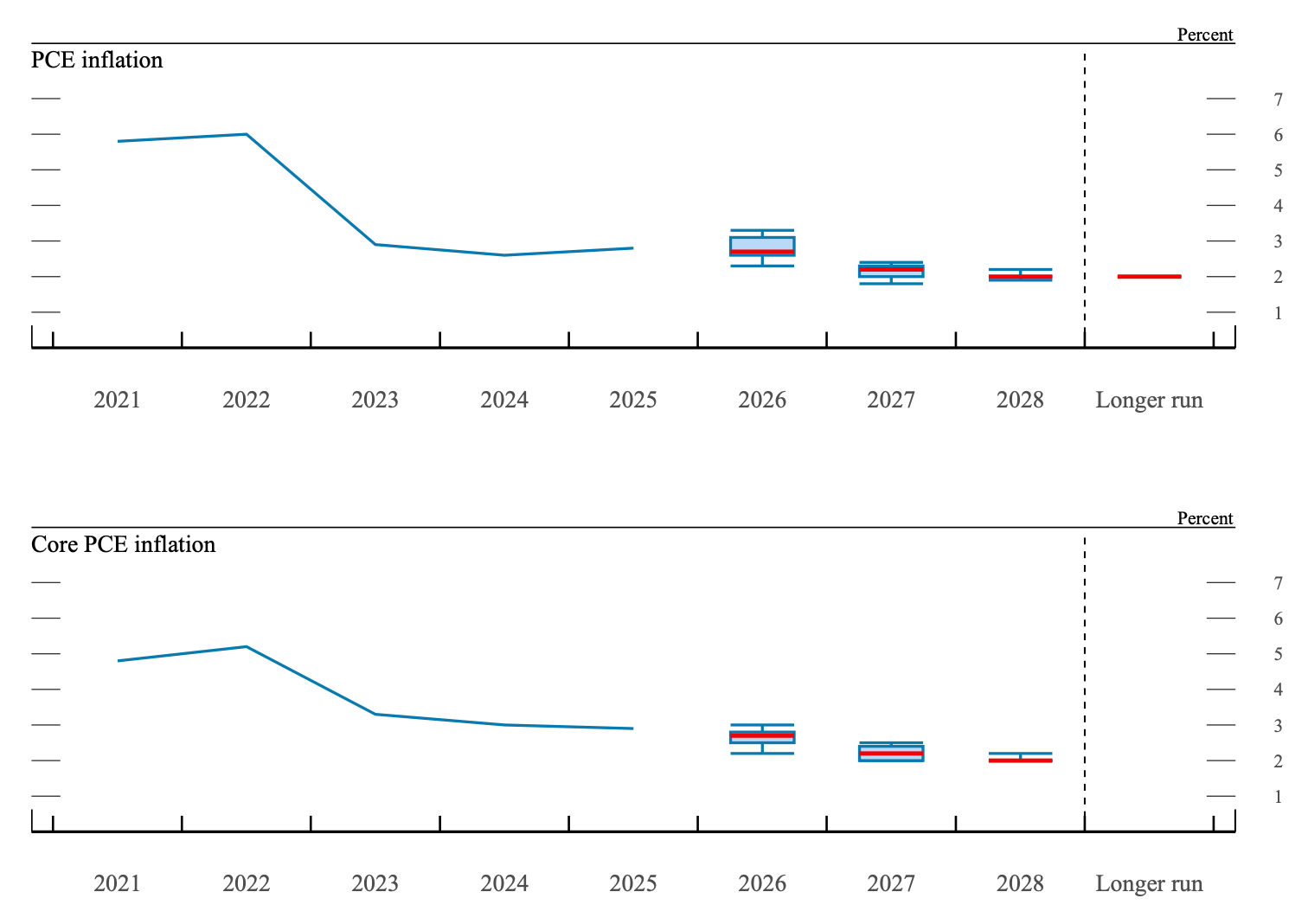

This is the most significant shift in the March projections. The median for headline PCE inflation in 2026 rose 0.3 percentage points to 2.7% (from 2.4% in December), the largest single-year upward revision in recent cycles. Core PCE inflation (excluding food and energy) was also marked up 0.2 percentage points to 2.7% for 2026 (from 2.5%).

| Year | March 2026 Median | December 2025 Median | Change |

|---|---|---|---|

| PCE | |||

| 2026 | 2.7% | 2.4% | +0.3 pp |

| 2027 | 2.2% | 2.1% | +0.1 pp |

| 2028 | 2.0% | 2.0% | unchanged |

| Longer run | 2.0% | 2.0% | unchanged |

| Core PCE | |||

| 2026 | 2.7% | 2.5% | +0.2 pp |

| 2027 | 2.2% | 2.1% | +0.1 pp |

| 2028 | 2.0% | 2.0% | unchanged |

Table 2. FOMC median PCE and core PCE prediction in March 2026 vs December 2025.

Smaller increases appear in 2027 medians (headline to 2.2%, core to 2.2%), while 2028 and longer-run projections remain anchored at 2.0%. The upward revisions suggest the Committee incorporated recent data showing stickier services prices and slower-than-expected disinflation, with the bump not viewed as purely energy-driven.

PCE and core PCE also experienced the highest redistribution of near-term predictions for 2026, towards much higher ranges, reflecting the latest accelerating PCE data and potentially inflationary trends: oil/shipment shock and tariffs.

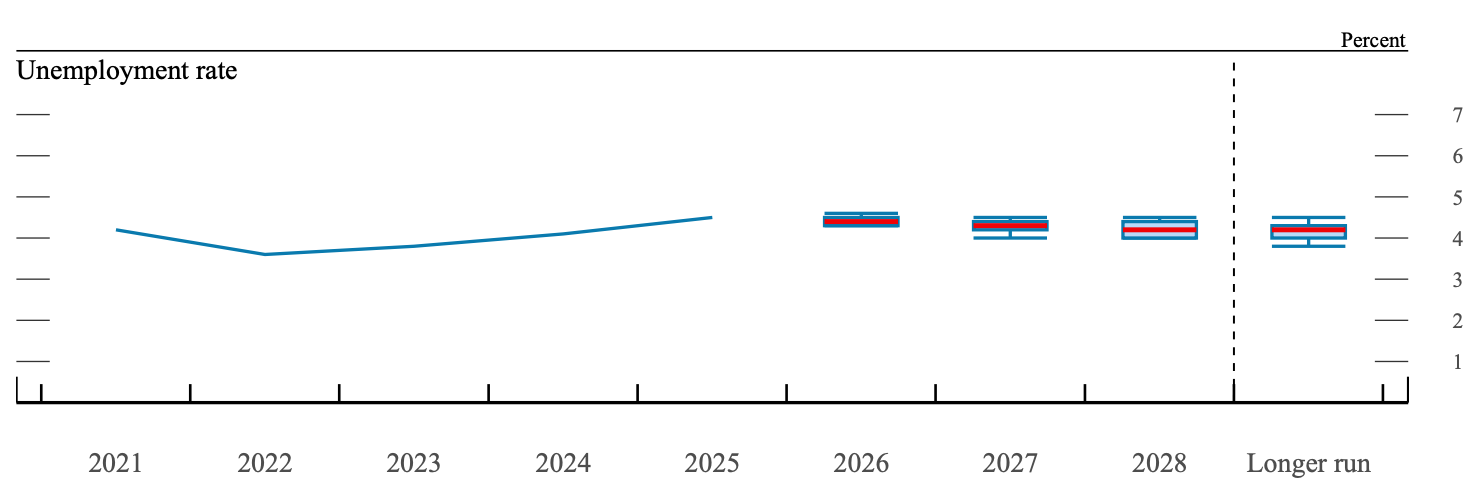

Unemployment Rate: Essentially Unchanged, Signaling Labor Market Stability

Projections for the civilian unemployment rate (Q4 average) show very little movement. The median remains at 4.4% for 2026 (unchanged from December), rises modestly to 4.3% for 2027 (from 4.2%), and holds at 4.2% for 2028 and the longer run.

| Year | March 2026 Median | December 2025 Median | Change |

|---|---|---|---|

| 2026 | 4.4% | 4.4% | unchanged |

| 2027 | 4.3% | 4.2% | +0.1 pp |

| 2028 | 4.2% | 4.2% | unchanged |

| Longer run | 4.2% | 4.2% | unchanged |

Table 3. FOMC unemployment rate predictions (Q4 average, percent) between March 2026 and December 2025.

This stability contrasts with the upgrades to growth and inflation, implying the Fed continues to view the labor market as resilient and near its estimated longer-run natural rate of 4.2%, with no material softening expected despite stronger growth forecasts.

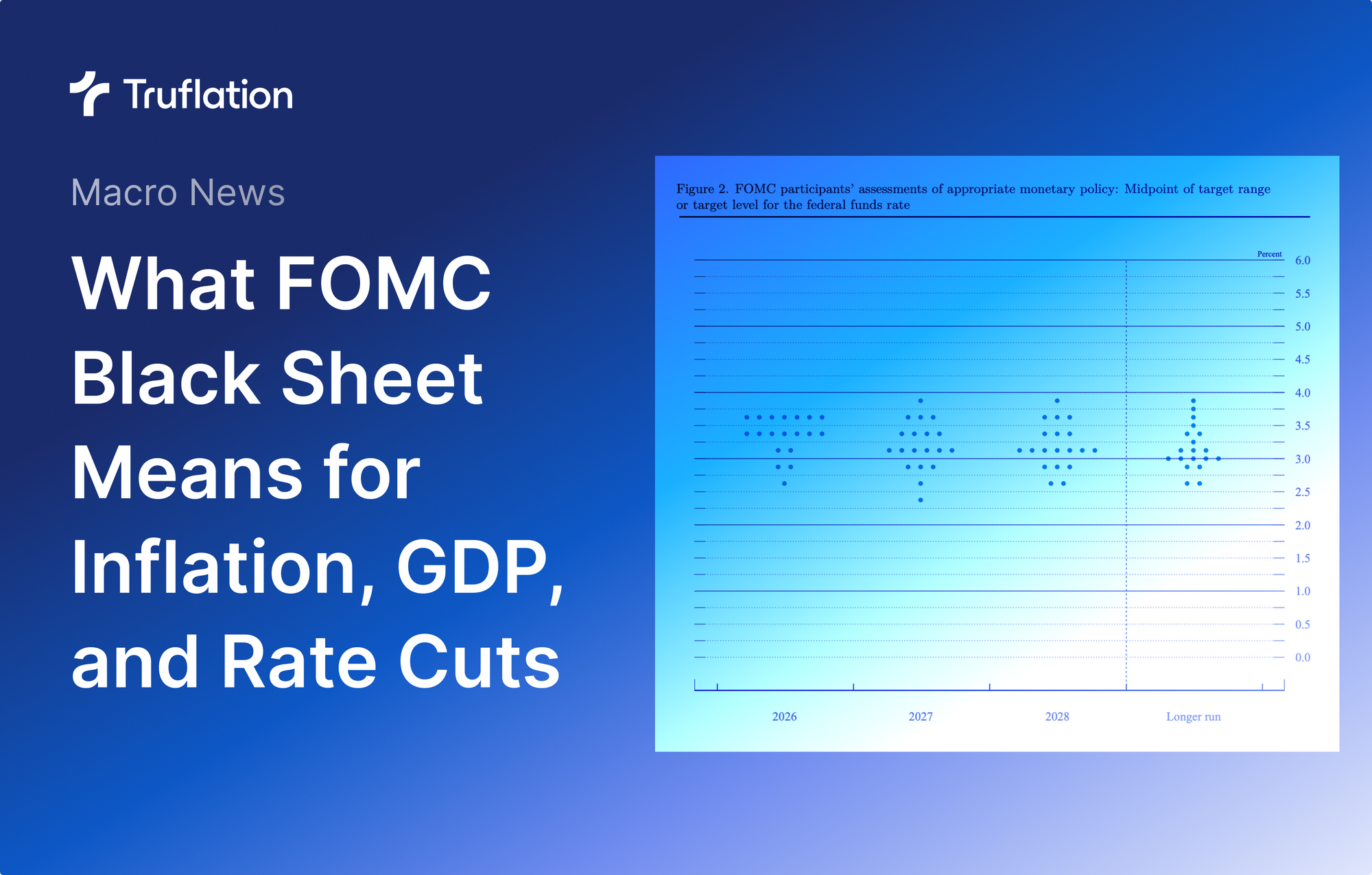

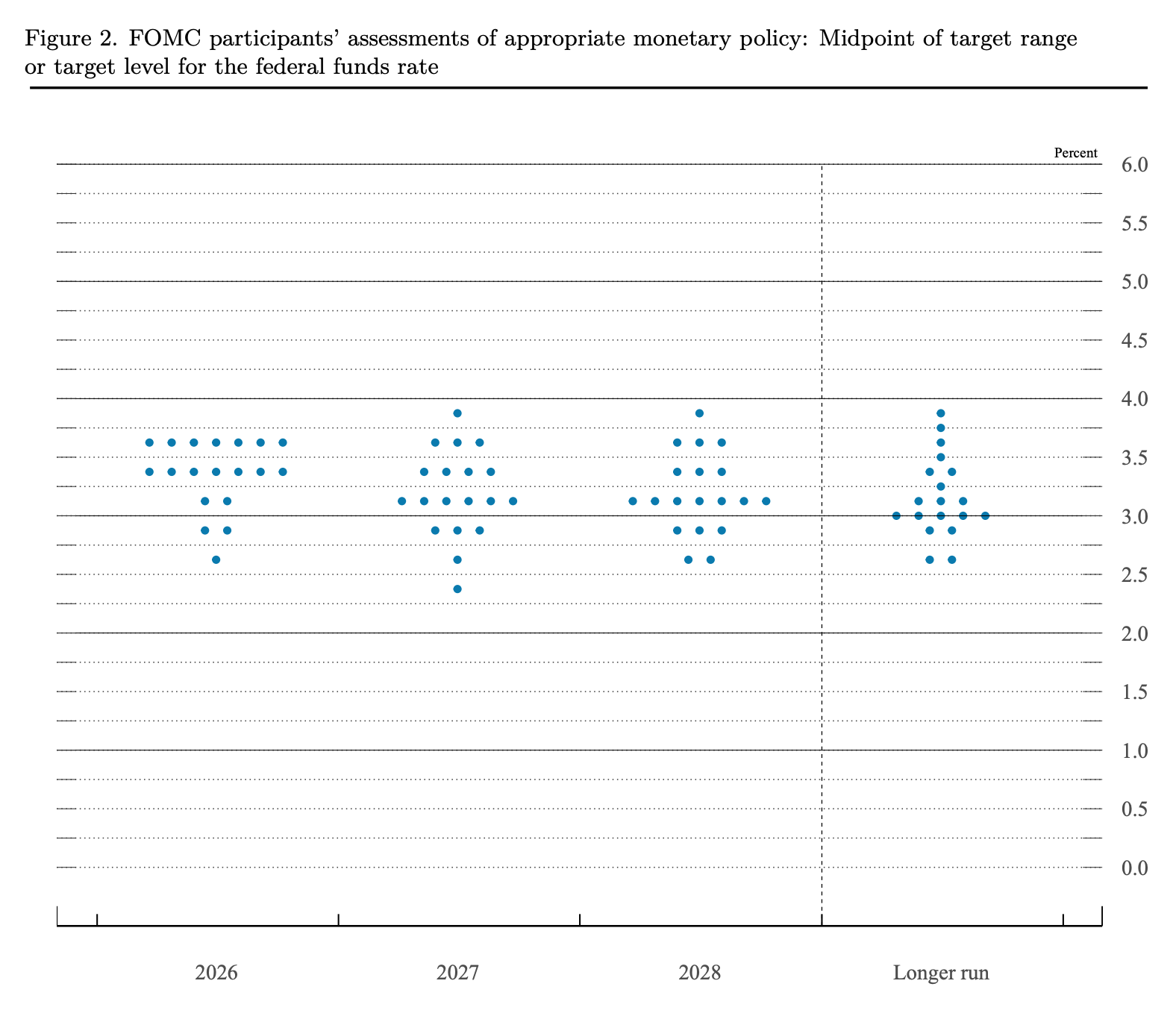

Federal Funds Rate Path: Unchanged Near-Term Median, One 25 bp Cut Implied for 2026

The median projected federal funds rate (end-of-year target midpoint) is unchanged at 3.4% for end-2026, 3.1% for 2027, and 3.1% for 2028. The longer-run neutral rate ticked up 0.1 percentage point to 3.1% (from 3.0%).

| Year | March 2026 Median | December 2025 Median | Change |

|---|---|---|---|

| 2026 | 3.4% | 3.4% | unchanged |

| 2027 | 3.1% | 3.1% | unchanged |

| 2028 | 3.1% | 3.1% | unchanged |

| Longer run | 3.1% | 3.0% | +0.1 pp |

Table 3. FOMC Federal funds rate predictions (Q4 average, percent) between March 2026 and December 2025.

With the current target range at 3.50%–3.75%, the 3.4% median for end-2026 implies approximately one 25-basis-point cut over the remainder of the year as the central expectation. Individual participant views show a relatively clustered distribution, with a clear majority projecting either no cuts or exactly one 25 bp cut in 2026, and only a small number anticipating two or more cuts.

Even though the forecasted target interest rates didn't change much between December and March, the small longer-run adjustment and the altered distribution of votes among the committee members, together with a much worse outlook for PCE inflation, led to a sharp hawkish repricing of market odds on Fed easing policies.

Uncertainty and Risks: Mild Increase, Concentrated in Inflation

Participants assessed uncertainty around their projections as broadly similar to or higher than the average of the past 20 years. The increase was modest overall and uneven: uncertainty around GDP growth and the unemployment rate rose only slightly, while assessments for both headline and core PCE inflation showed a clearer rise in perceived uncertainty.

On the balance of risks, views remain broadly balanced across variables, but a modest tilt toward upside inflation risks emerged, consistent with the higher near-term PCE forecasts. This nuanced shift helps explain the Fed’s cautious policy path despite the stronger growth outlook.

What It Means for Markets and Inflation Watchers

- Growth: The modestly stronger GDP projections reduce recession concerns but also make the Fed less inclined to deliver aggressive rate cuts.

- Inflation: The 0.3 percentage-point upward revision to the 2026 headline PCE is the key takeaway. It signals that disinflation is likely to take longer than the FOMC members hoped in December 2025, aligning with recent higher sticky core readings from the BEA PCE.

- Policy: The median rate-cut path continues to point to gradual easing, with roughly one 25 bp cut priced in for 2026 and one for 2027. Higher and sticker inflation predictions give more fuel to the Fed's favorite “higher for longer” stance.

The next SEP update will follow the June 2026 FOMC meeting. In the interim, monthly PCE, CPI, and labor market data releases remain critical to the Fed's policy decisions.