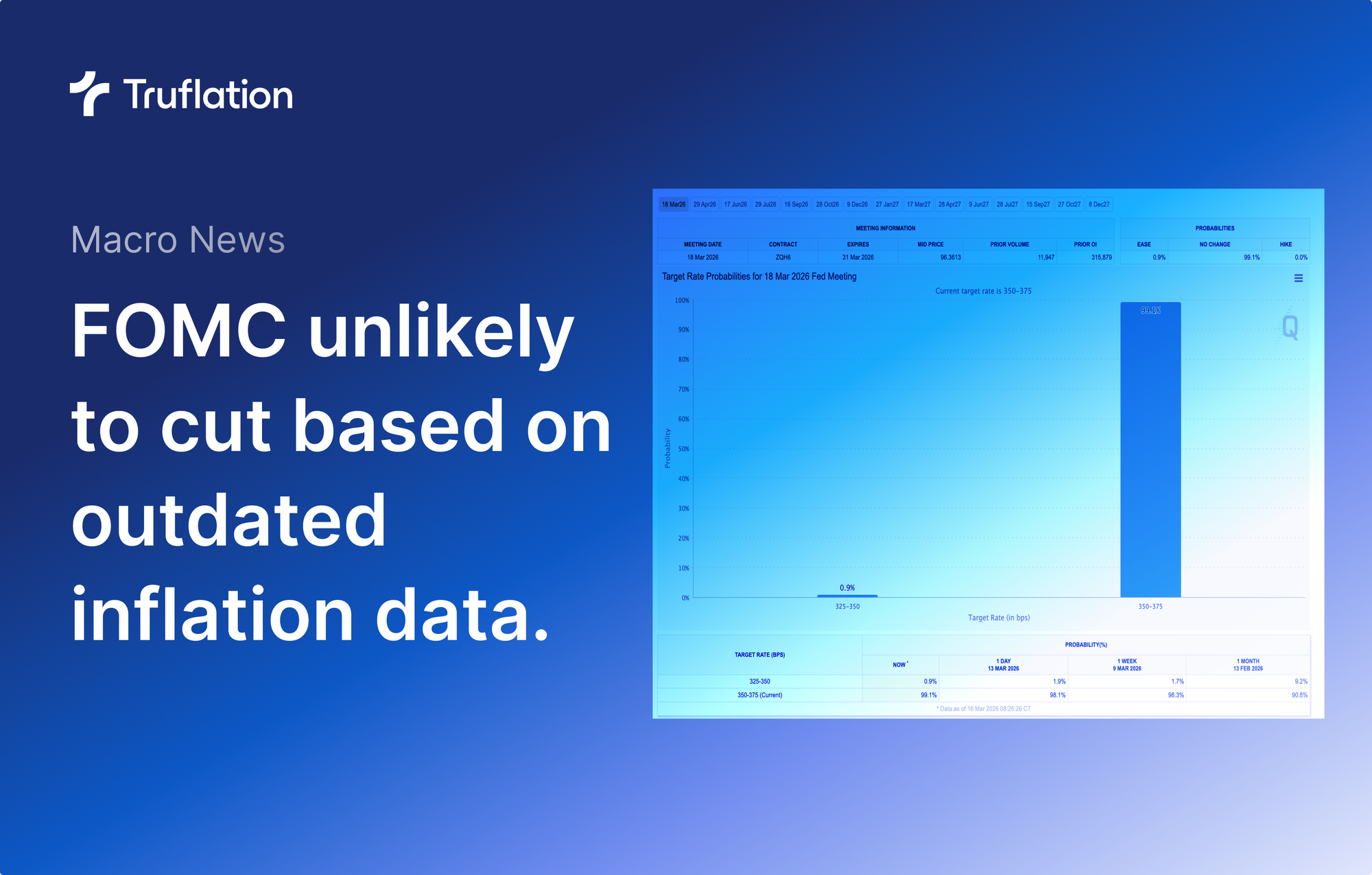

FOMC not expected to cut rates based on outdated CPI and PCE data.

Tomorrow, March 17, the Fed starts its March FOMC meeting with the final interest-rate decision on Wednesday, March 18.

Markets expect interest rates to remain unchanged in the 3.5%-3.75% range (350-375 bps) for this and the next FOMC meeting. This has been the case since at least January, so no big surprises there. FedWatch also shows a low chance of cuts during the next two meetings.

Additionally, the latest official CPI, PCE, and labor data show little change, meaning official inflation is slow to drop to the Fed's target range of 2%, while the labor market shows stagnation but without clear signs of breaking, with low new job openings but also low turnover and unemployment, which all support a 'wait and see' approach and a continued pause on cuts.

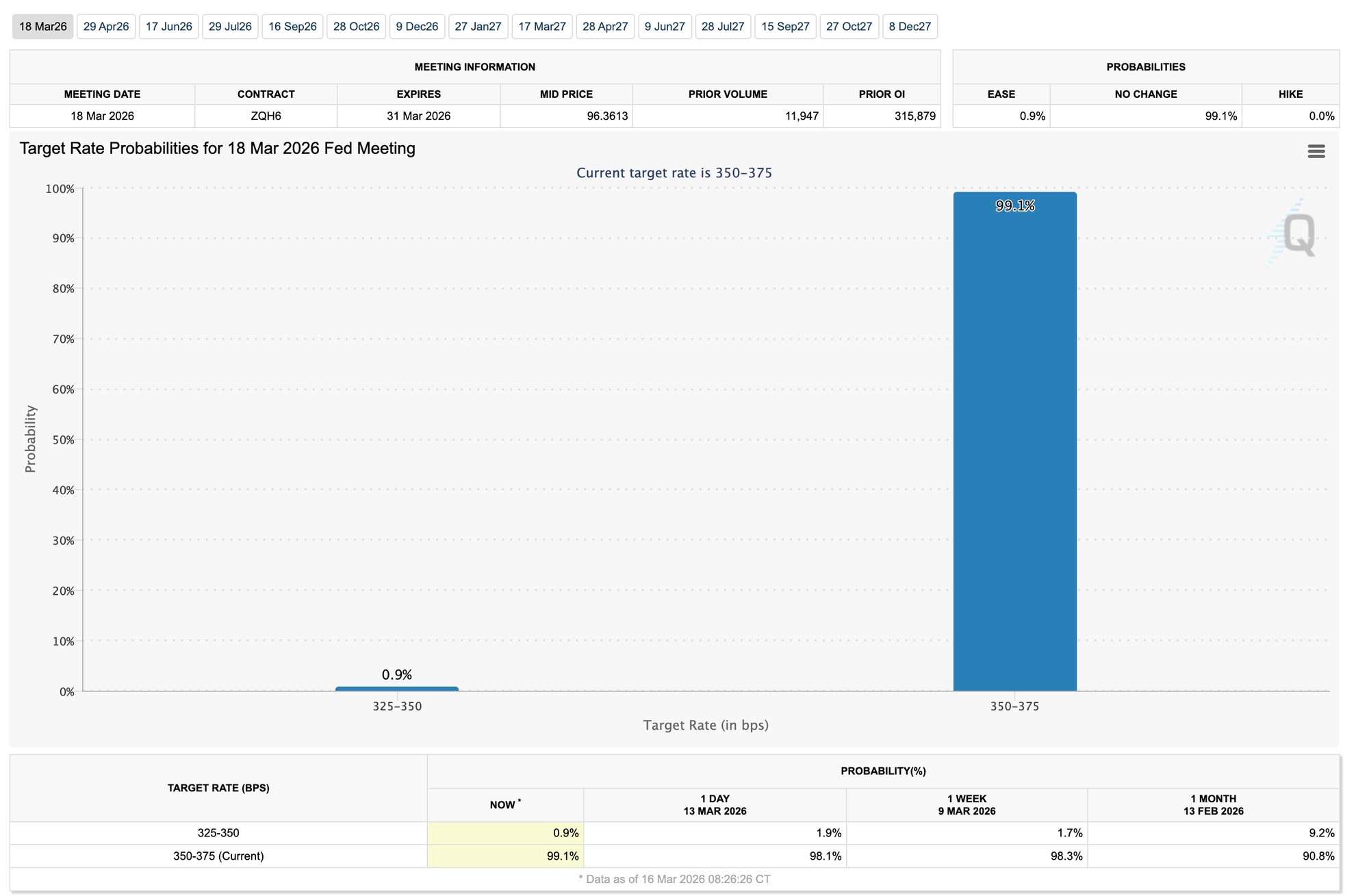

We covered the latest government releases for February CPI (2.4% Y/Y) and January PCE (2.8% Y/Y) in our news.

This upcoming FOMC meeting will be interesting mainly for gauging the Fed's 2026 outlook and signs of potential dissent.

This year, we'll also see Jerome Powell stepping down as Fed chair in mid-May and the Senate approval of the new chair, which we covered extensively in our latest inflation report.

2026 FOMC cuts are not looking promising

For the whole of 2026, top commercial bank analysts expected only between 0 and 3 cuts of from 0 to 75 bps (0.75%), with City Bank most optimistic, and JP Morgan expecting no cuts.

This means markets could see zero cuts this year, especially if data remains stable with inflation still above the 2% target, while the labor market shows no signs of breaking (just yet).

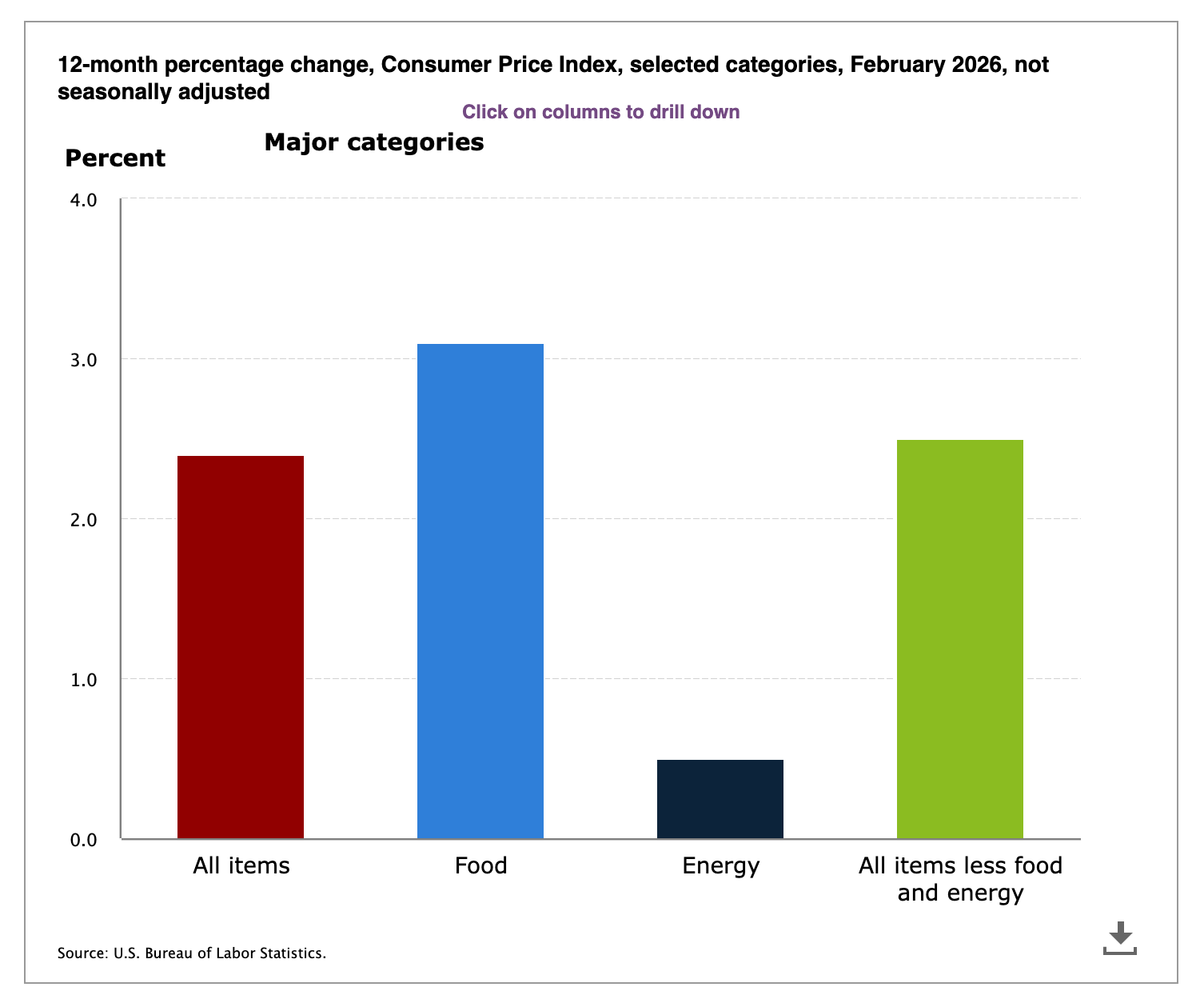

So far this year, the Federal Reserve hasn't cut rates. The Fed cut 3 times in 2025 and 3 times in 2024. The last cuts we saw in December were likely prompted by worsening labor statistics and a sudden panic in the bond market. The Fed might indeed be waiting for part of its dual mandate or something serious in the markets to break before the next cut.

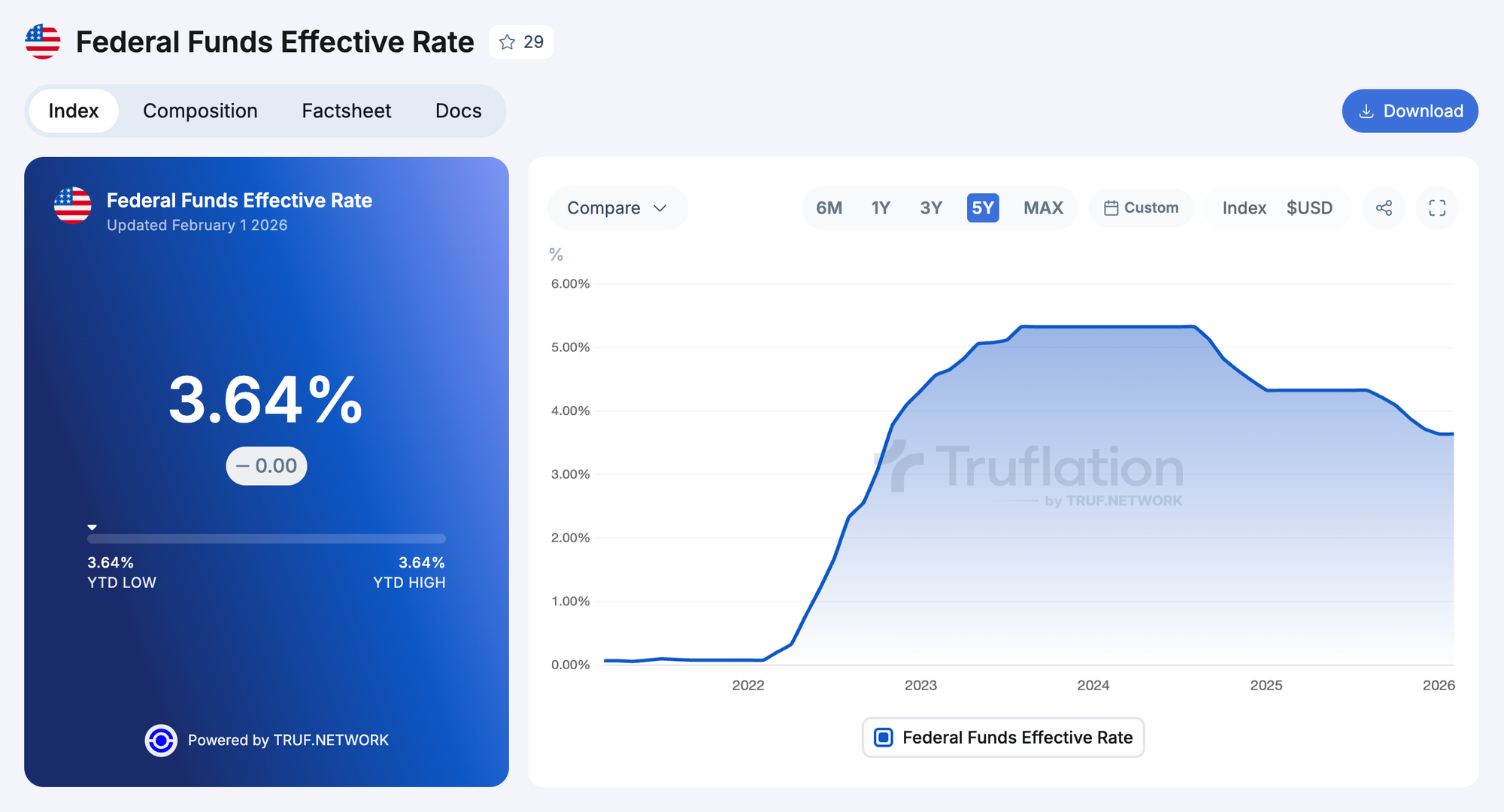

The Effective Federal Funds Rate (EFFR) – the actual weighted-average rate of overnight loans between banks, calculated daily based on real transactions – fluctuated a bit more, dropping to 3.64% in Feb 2026. The EFFR is calculated based on the FOMC target range and typically falls within it.

Real-time CPI data still below 2%

Almost all Fed officials point to inflation above 2% as their main reason for not cutting interest rates and continue quoting BLS CPI and BEA PCE inflation data.

Both of those official sources have been shown to be outdated in multiple research papers by Penn State University and by prominent economic analysts. The BLS and BEA indexes, especially their rent indexes, carry inherent delays of a few months. They are also released with a 1-2 month lag relative to real-time transaction data, which Truflation aggregates daily and uses to calculate our CPI and PCE alternatives.

Read our latest report on how Truflation precedes the official CPI data by at least 45 days.

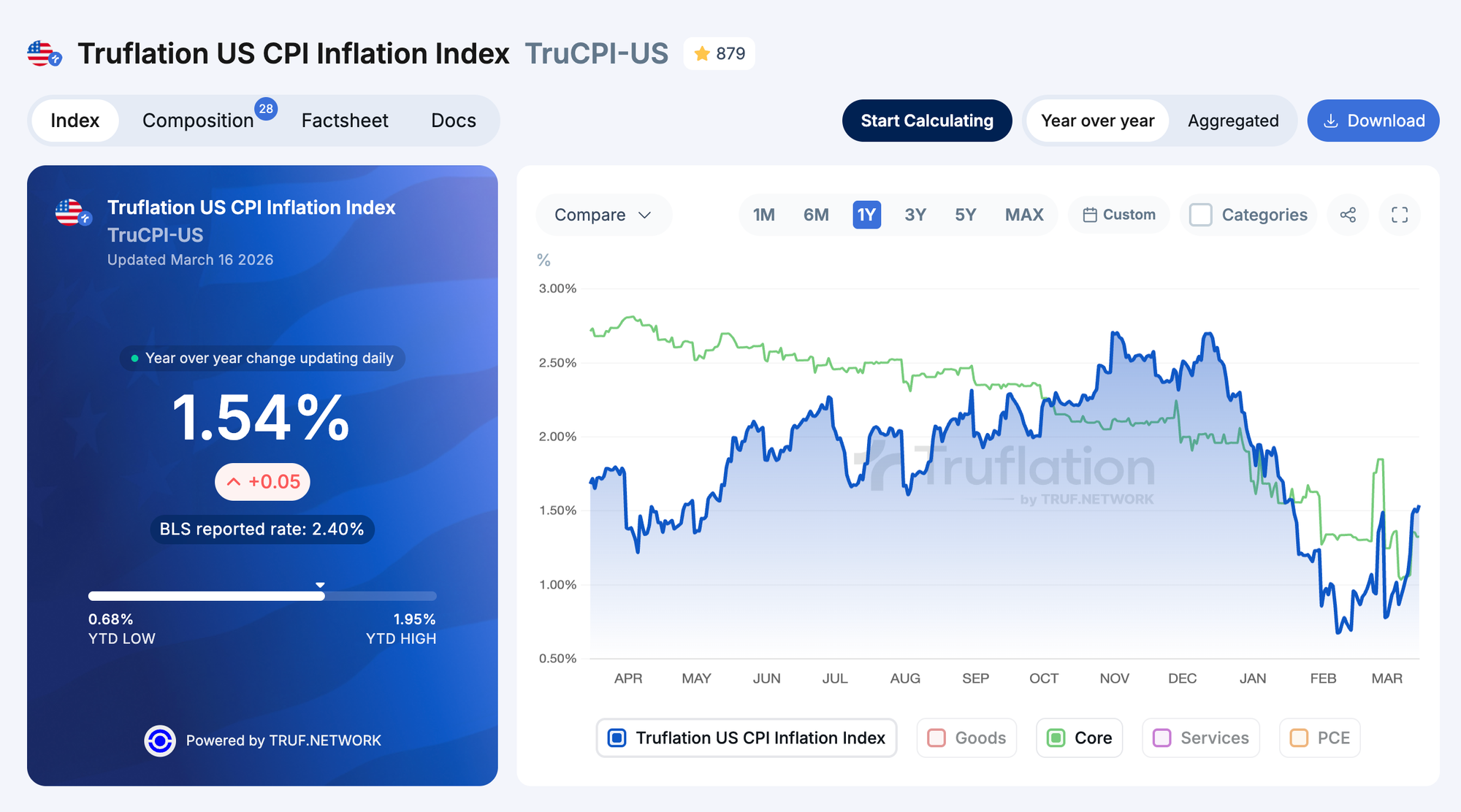

The real-time inflation calculated by Truflation, based on actual transaction prices, dropped significantly below the Fed's 2% target in January and February 2026, before bouncing back slightly, but still below 2%, in March.

- Trulation US CPI was 1.54% Y/Y (as of March 16)

- Truflation core US CPI was 1.33% Y/Y (as of March 16)

The core CPI, which excludes volatile food and energy, was lower than the headline at 1.33% (as of March 16) and may still be in a downtrend, suggesting that the latest upward gains are likely temporary and driven by the oil price and shipping costs related to the conflict in the Middle East.

This doesn't mean we call for the Fed to cut rates, though many prominent economists and analysts who use our data do. We only point out that more accurate and real-time inflation is already below 2%, and if the Fed were using Truflation, they could have cut as far back as Q1-Q2 2025.

Data shows inflation dipped below the 2% target for months in 2025 and in January and March 2026. The short uptick in CPI inflation in Q4 2025 stemmed mainly from the +0.7 added temporarily by tariffs and since then completely priced in, as estimated by our data team and covered in the December report and January inflation report.

Alternative PCE data now climbing back up

The real-time PCE index, which we obtain by mapping our transaction data onto the BEA weighting and categories, has jumped significantly in March 2026, while the core PCE continued to drop or stay flat, suggesting a much stronger influence from volatile food and energy items.

- Trulation US PCE today was 2.4% Y/Y

- Truflation core US PCE today is 2.4% Y/Y

Official PCE and especially core PCE is often called the Fed's favorite gauge of inflation, and it's been particularly slow to come down; even our PCE is now running hot, above 2%. If there had been a good window for the Fed to cut rates more aggressively, it might have passed. The current oil and shipping crisis in the Middle East has broader inflationary effects, and everything will depend on how long it lasts.