The Conference Board Consumer Confidence Report – March 2026

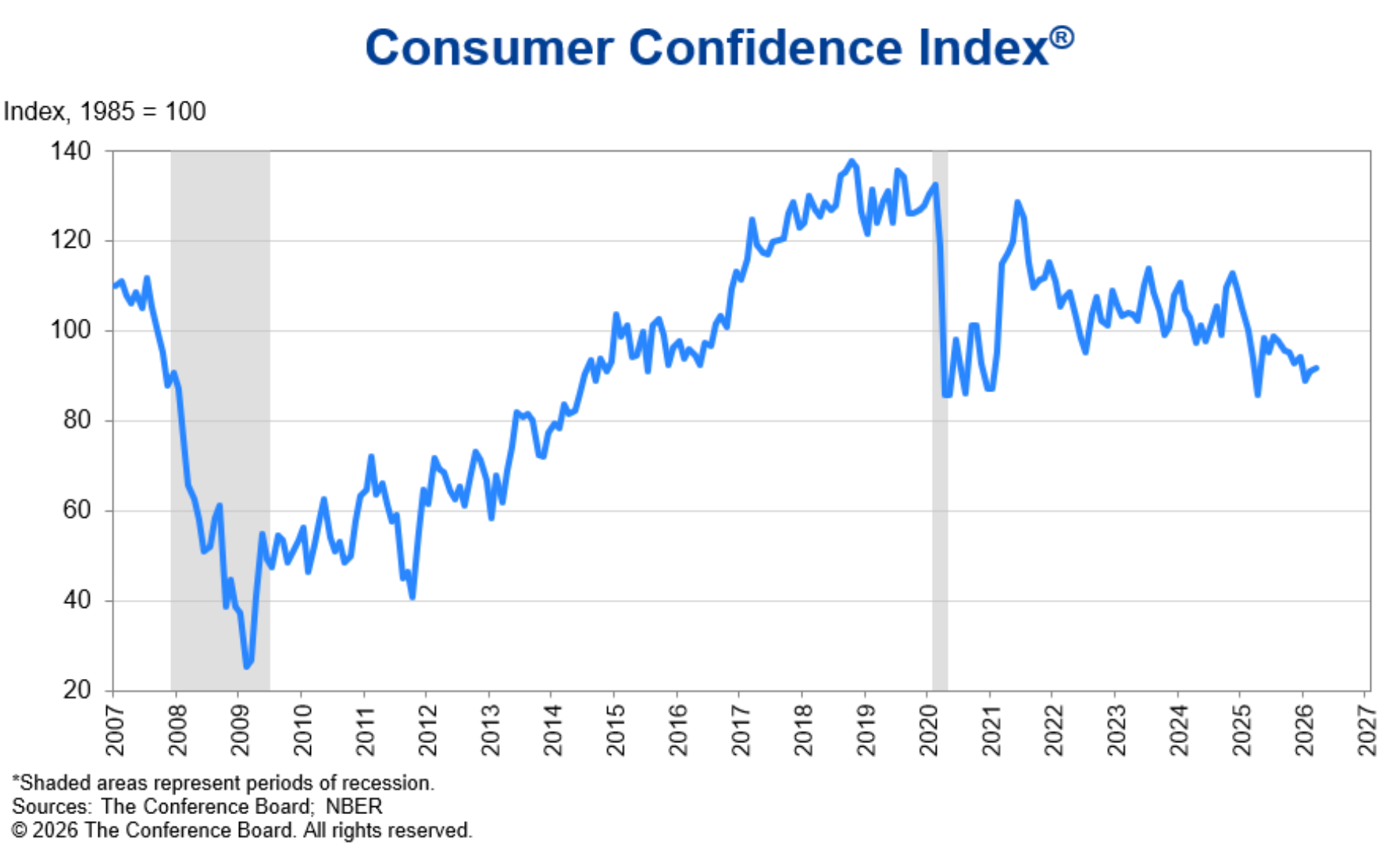

The Conference Board Consumer Confidence Index edged higher to 91.8 in March (from 91.0), beating expectations of 87.8. This marks the second consecutive modest gain in consumer confidence. However, the index remains on a general downward trajectory observed since 2021 and sits well below pre-pandemic averages

Despite surging costs from tariffs and elevated energy prices (as reflected in higher inflation expectations), consumers viewed the current environment more favorably.

This report supports near-term spending resilience but signals caution ahead. Reinforces higher-for-longer rates with 10Y yield near 4.31%. Risk assets remain sensitive.

The components of the Consumer Confidence Index:

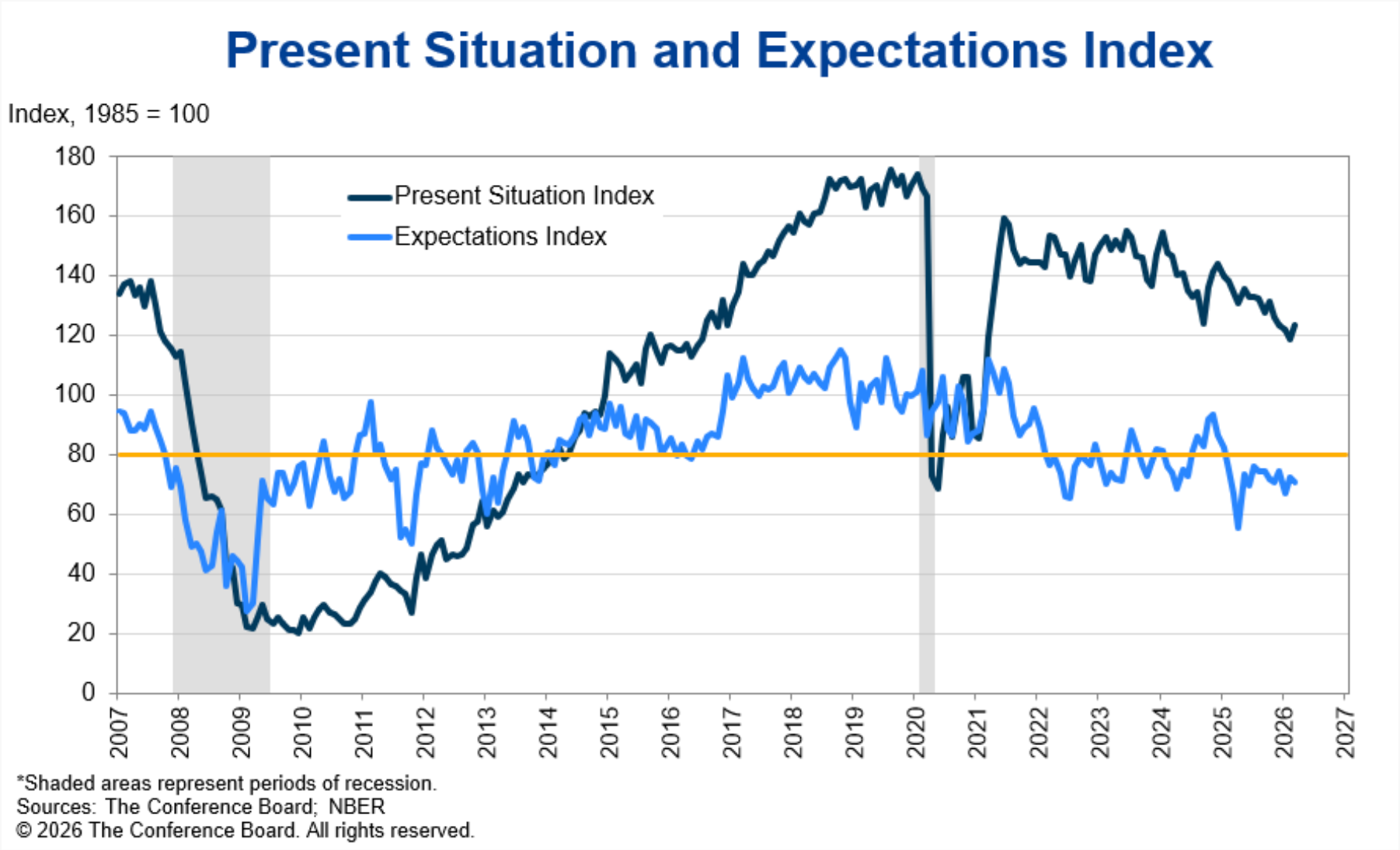

Present Situation Index increased +4.6 pts to 123.3, driving the headline confidence, signaling more positive assessments of current business and labor conditions.

- Net view of current business conditions rose to +5.6% (from near 1-2% in recent months).

- 21.9% of respondents rated business conditions “good” (up from 20.4%).

- 16.3% rated them “bad” (down from 19.0%).

- Labor market differential (jobs “plentiful” minus “hard to get”) edged higher by 0.1 ppt to +5.8%, indicating slightly firmer employment perceptions despite broader economic headwinds.

Expectations Index eased -1.7 pts to 70.9, reflecting caution over the near-term outlook. This forward-looking gauge, covering short-term outlooks for income, business, and labor conditions, remains deeply pessimistic and below the 80 threshold often associated with recession risks.

- Two of three components weakened: net perceptions of future labor market and household income conditions softened.

- Expected business conditions six months ahead showed a slight improvement, but stayed negative overall.

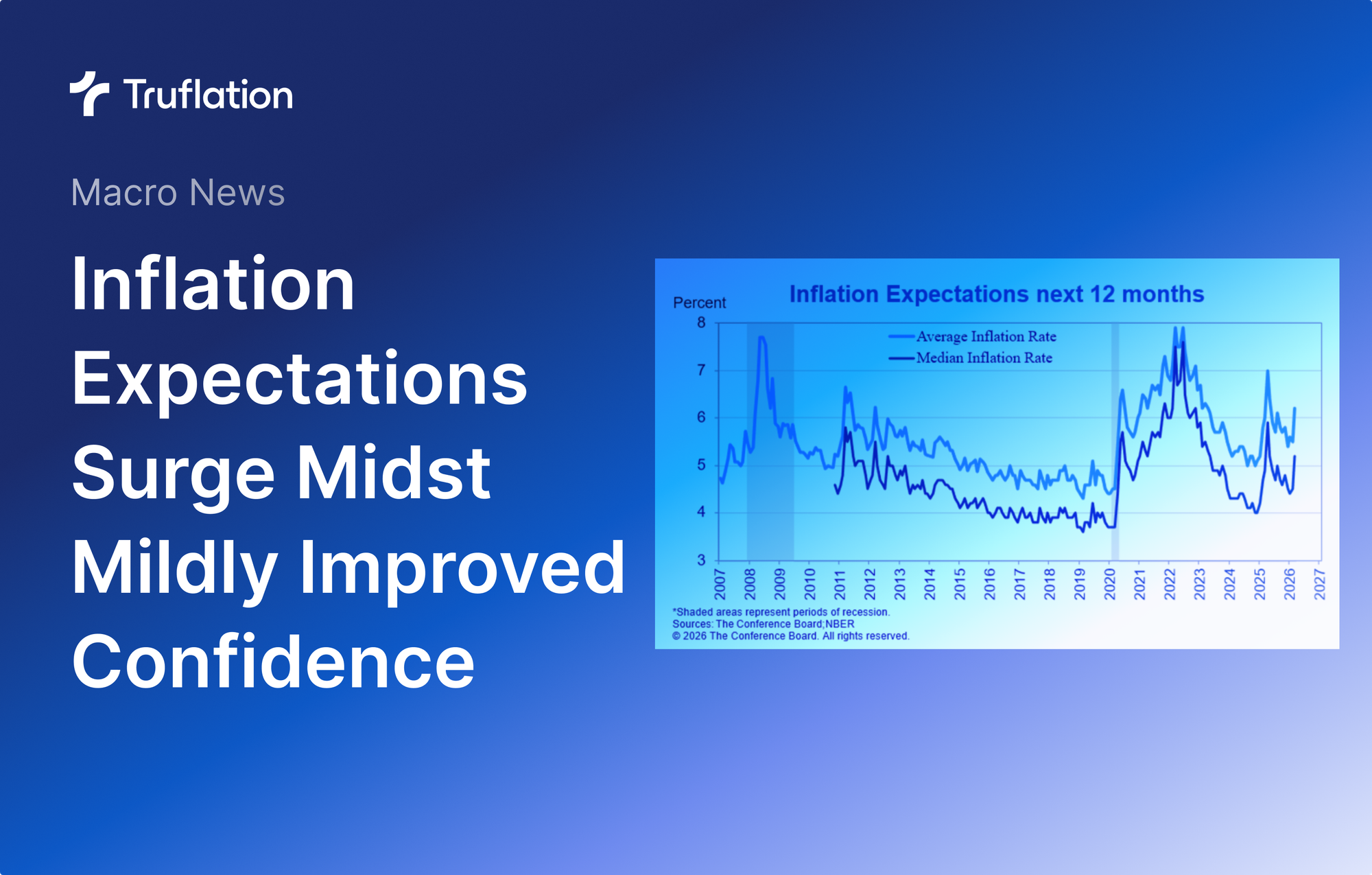

The Conference Board Inflation Expectations and Cost Pressures:

The Consumer Confidence survey period (March 1–24) captured the early impact of tariff passthrough and the oil price shock linked to geopolitical tensions (Iran war).

While not fully visible in the headline or main sub-indices, these pressures were evident in supplementary measures, especially Inflation Expectations.

- Consumers’ average and median 12-month inflation expectations surged to levels last seen in August 2025, when tariff announcements were pending.

- Comments highlighted the cost of living as a top concern, with rising prices for goods and gasoline remaining front-of-mind.

To summarize the Consumer Board Report, Chief Economist Dana Peterson noted:

“Consumer confidence ticked up again in March, as a modest improvement in consumers’ views of current conditions outweighed a slight downshift in expectations for the future… Nonetheless, the index has been on a general downward trend since 2021.”

Market and Economic Implications

- Consumer Spending: The firmer Present Situation Index supports near-term resilience in spending, particularly on essentials and limited discretionary items. However, the weak Expectations Index and elevated inflation expectations signal caution, likely constraining big-ticket and discretionary outlays in Q2–Q3.

- Labor Market: Mildly positive job perceptions align with recent JOLTS data but do not override broader tightness concerns.

- Policy Outlook: Persistent cost pressures and higher inflation expectations reinforce a higher-for-longer Fed stance. This keeps upward pressure on Treasury yields (10Y near 4.31–4.44%) and tightens financial conditions.

- Risk Assets: Equities and crypto remain vulnerable to any further inflation repricing or escalation in energy/geopolitical risks. Bitcoin’s recent trading near $66,700 reflects this sensitivity.

- Broader Context: The divergence with the University of Michigan Consumer Sentiment Index (final March reading at 53.3, sharply lower) underscores mixed consumer signals amid energy volatility.