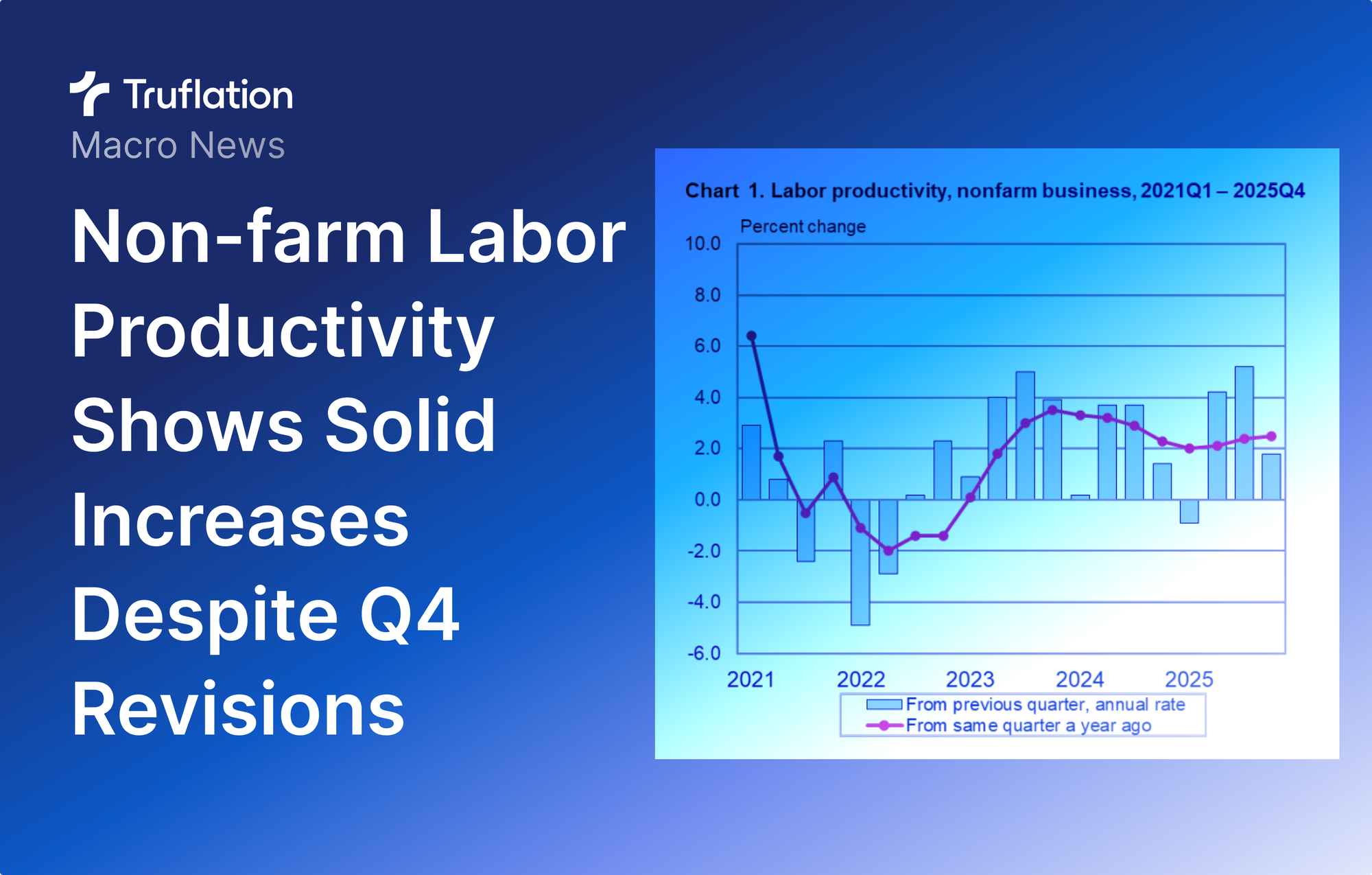

Labor Productivity Shows Solid Increase Despite Q4 Revisions

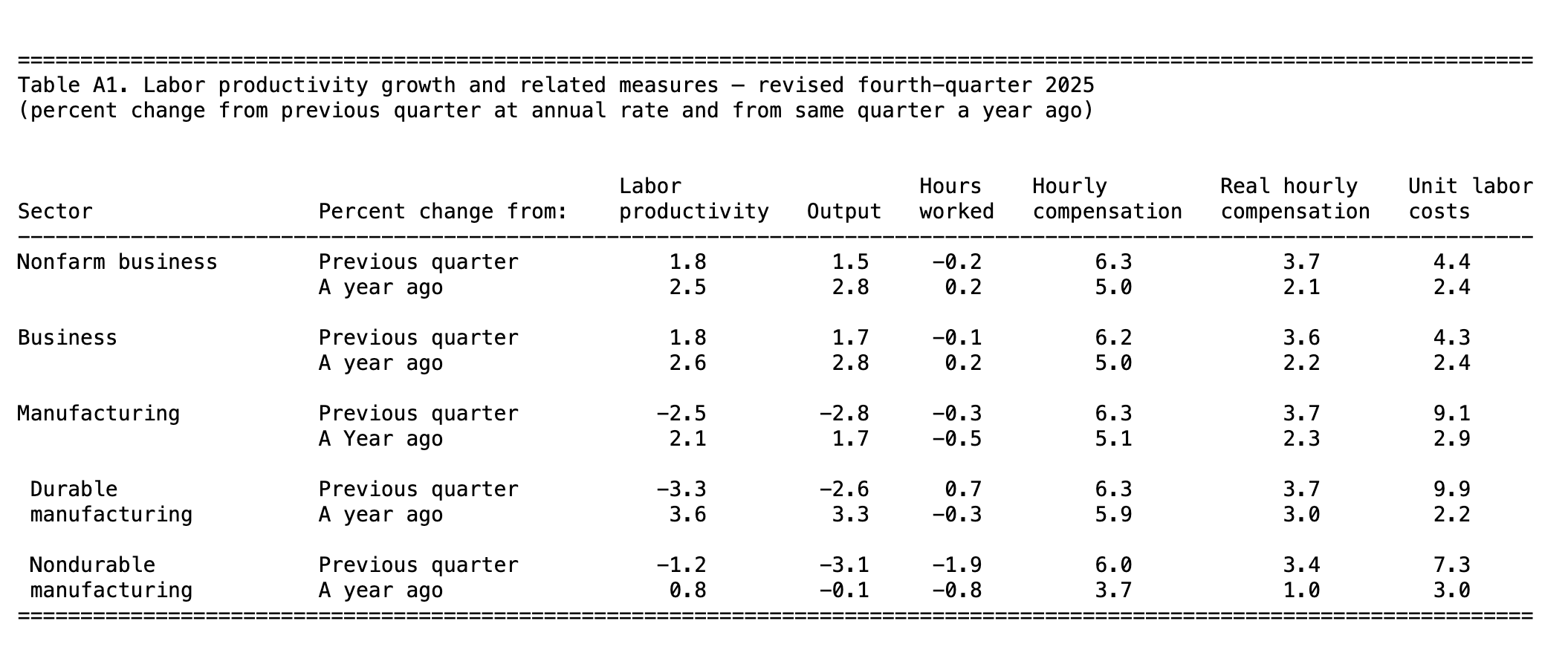

Today, the BLS released its revised Productivity & Costs report for Q4 2025 (Revised) and 2025 Annual Averages. Nonfarm business sector rose 1.8% annualized in Q4 2025 (down from the preliminary 2.8% estimate), as real output grew 1.5% while hours worked edged down 0.2%. Year-over-year, productivity was up 2.5%. For the full year 2025, productivity advanced 2.1%.

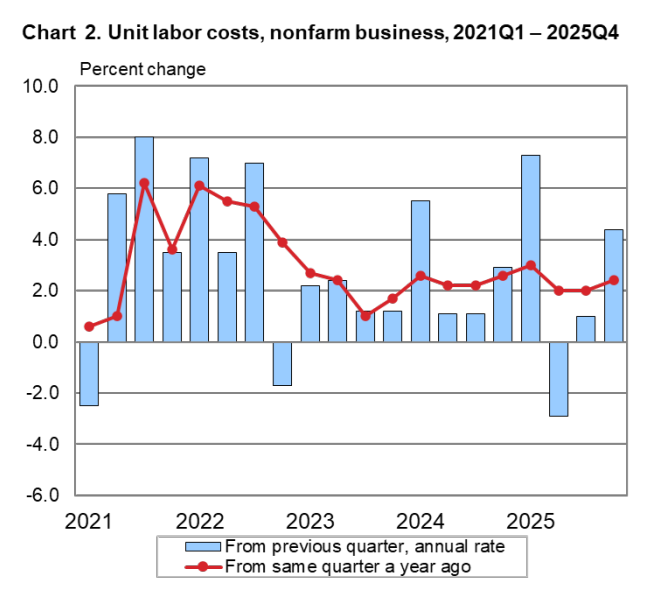

Unit labor costs accelerated sharply to +4.4% in Q4 (revised up from 2.8%), driven by hourly compensation rising 6.3% while productivity came in softer. Real (inflation-adjusted) hourly compensation still increased a healthy 3.7%. Annual unit labor costs rose 2.3%.

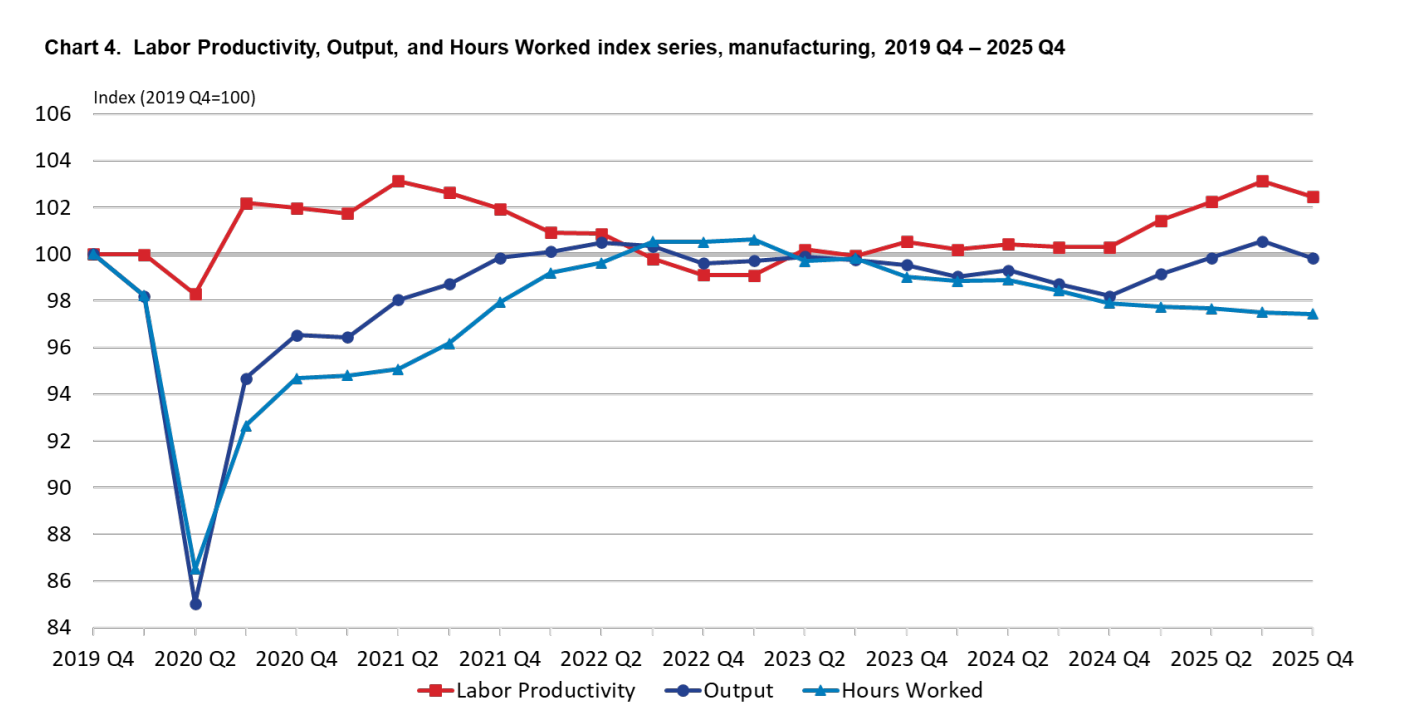

Manufacturing painted a weaker picture: productivity fell 2.5% in Q4 (output –2.8%), pushing unit labor costs up 9.1%, the largest quarterly jump since Q3 2022. On an annual basis, however, manufacturing productivity rose 1.9%, the strongest year since 2010.

What This Means for the US Economy

- Positive signal: 2025 delivered above-trend productivity growth (2.1%), supporting the economy’s ability to grow without generating excessive inflation. The cycle-average since Q4 2019 now stands at 2.1% annualized, better than the prior cycle.

- Cautionary note: The downward revision to Q4 productivity and upward revision to unit labor costs highlight that wage pressures outpaced efficiency gains late last year. If this pattern persists, it could keep underlying cost pressures alive.

- Inflation outlook: Moderating productivity surprises can make it harder for the Fed to declare victory on inflation, as firms pass on higher unit labor costs to consumers. However, the still-positive real wage growth supports consumer spending.

Market Implications

Stocks: Mixed. Solid annual productivity is fundamentally bullish for corporate margins and earnings growth over time, but the Q4 softening and rising unit costs may temper near-term optimism, especially in rate-sensitive sectors.

Bonds: The jump in Q4 unit labor costs adds a mild hawkish tilt. It reduces the urgency for aggressive Fed rate cuts, supporting higher-for-longer yields and putting modest upward pressure on Treasury yields.

Crypto & Risk Assets: Productivity is a long-term tailwind for risk appetite (more output per worker = higher potential growth). Short-term, however, stickier cost pressures could keep volatility elevated if they feed into persistent inflation expectations.

Currencies & Commodities: A resilient productivity backdrop supports the USD. Energy and industrial commodities remain sensitive to any signs that manufacturing weakness is broadening.

Overall, 2025’s 2.1% productivity gain is encouraging for potential GDP growth, but today’s revisions remind us that efficiency improvements are not accelerating as strongly as initially thought. Sustained wage growth without matching productivity could keep inflation elevated for longer, so we will continue to monitor Q1 2026 data closely. We are also working on an independent wage index that would shed more light on the real-time labor costs.