Urea, Fertilizer, and Food Prices. More Inflation on the Horizon?

Urea Supply Disruptions 2026: Geopolitics Just Turned Fertilizer into a Major Inflation Risk

As macro analysts tracking inflation dynamics through the Truflation lens, we’re always watching commodity supply shocks that hit agricultural input costs, food CPI components, and broader market volatility head-on.

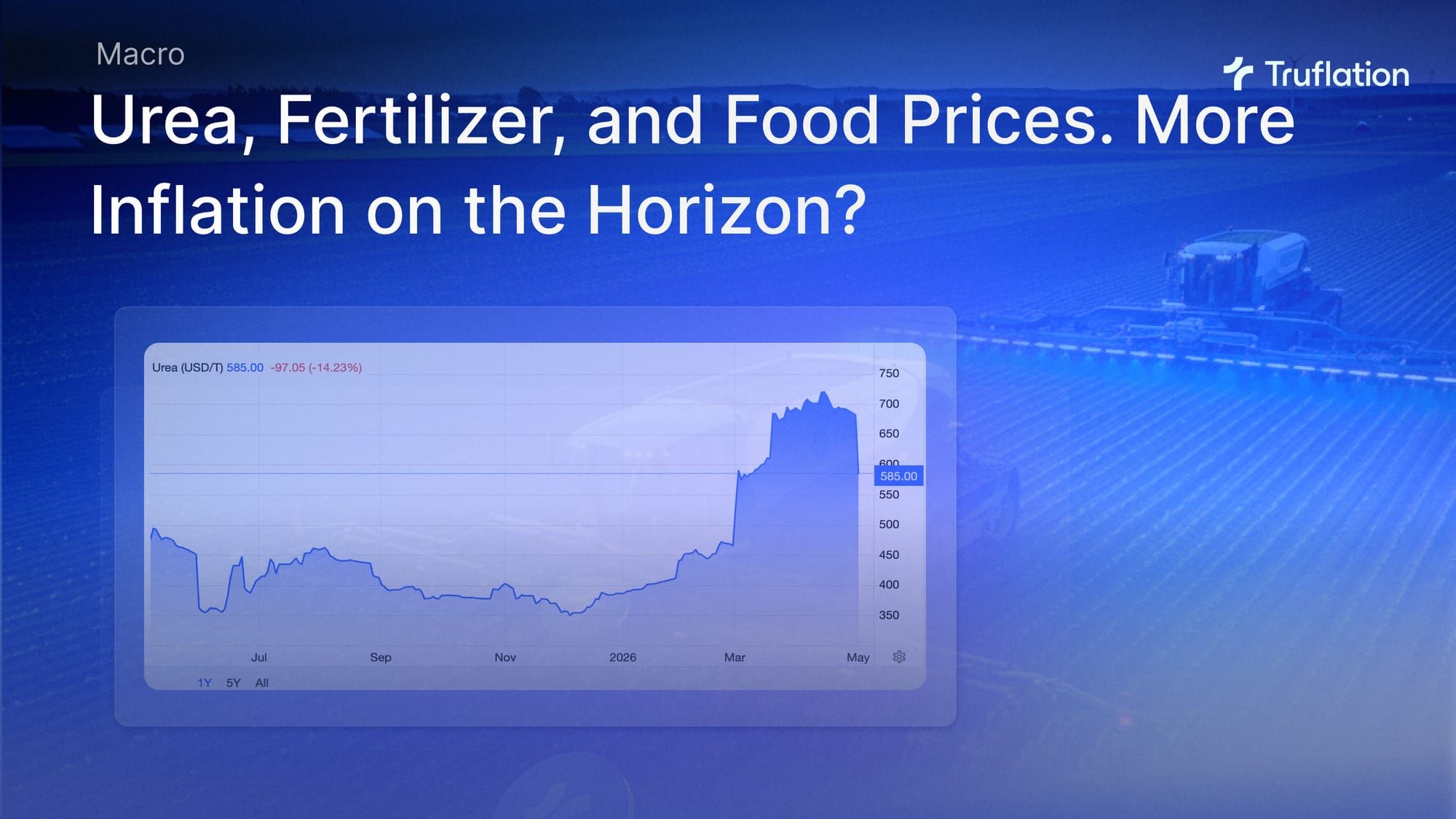

Right now, the urea market stands out as one of the sharpest near-term risks to global food security and inflationary paths heading into the Northern Hemisphere planting season. Since the start of the Iran conflict, the price of urea has nearly doubled, right into the spring planting season. And despite some recent drops, its ties to energy and geopolitics keep the risks high.

Here's a breakdown of the fundamentals:

What Is Urea and Why Does It Matter?

Urea (chemically carbamide, CO(NH₂)₂) is the world’s go-to nitrogen fertilizer. It packs about 46% nitrogen in an easy-to-handle granular form that farmers spread across huge acreages. It’s made by reacting ammonia (NH₃) with carbon dioxide under high pressure and temperature. Ammonia itself comes from the energy-hungry Haber-Bosch process, which in most major producing regions runs on natural gas (China being the big coal-based exception). That direct tie to hydrocarbon energy means urea supply is extremely sensitive to natural gas prices, availability, and any logistical bottlenecks.

Fertilizer use accounts for over 70% of global urea consumption, so when this market tightens, the ripple effects hit crop yields and food prices fast.

The Old Supply Picture – and Who Dominates It

The global urea trade has long been concentrated among a few low-cost natural gas producers. Russia has been the single biggest exporter, moving roughly 7–10 million metric tons a year into the U.S., Brazil, and India. The Middle East (Qatar, Saudi Arabia, Iran, UAE, Oman) is the heavyweight region, shipping about 20 million tons annually and handling 30–46% of all seaborne urea and nitrogen fertilizer.

Other key suppliers include Egypt, Algeria, and sometimes China (a top producer that usually keeps most output at home). Capacity was slated to grow through 2026 in the U.S., Russia, Qatar, and Nigeria, but geopolitics has already thrown a wrench in those plans.

Geopolitical tensions with Russia and the blockage of the Strait of Hormuz stopping anything coming from the Middle East, are what's driving the supply issues and prices right now.

What’s Breaking Right Now (May 2026 Update)

As mentioned, the price of urea has nearly doubled since the end of February. The big driver is the Iran conflict that escalated in late February 2026 and effectively shut down the Strait of Hormuz. That narrow waterway normally carries about one-third of globally traded urea and up to 40% of nitrogen fertilizer shipments. Persian Gulf plants—home to Qatar’s QAFCO (the planet’s largest single-site urea exporter), plus Saudi, Iranian, and Emirati facilities—have been hammered by gas supply cuts, plant shutdowns, and paralyzed shipping. Transit volumes through the strait have dropped more than 95% from pre-conflict levels, stranding millions of tons and sending prices soaring.

It doesn’t stop there:

- China ramped up export controls and customs inspections on urea and fertilizers starting in March 2026 to protect domestic stocks amid widening price gaps. Their already-tight quota system has basically taken a major swing supplier off the global board.

- Russia still runs some domestic-stabilization export quotas from 2025 but has kept deliveries flowing (it even became the top nitrogen fertilizer supplier to the U.S. in 2025). Port limits and policy caps keep it from scaling dramatically.

- Western sanctions on Russia have largely spared the fertilizer sector, so some continuity remains, but broader tensions add extra friction.

The combined effect—Hormuz blockade, Chinese restrictions, and Gulf production halts—has tightened the global urea balance far more quickly and harshly than anyone expected at the start of the year.

Can the U.S. or Europe Just Make More at Home?

The United States is in relatively good shape thanks to cheap shale gas on the Gulf Coast. Producers like CF Industries and Nutrien keep strong ammonia and UAN output running, so the U.S. is largely self-sufficient in those areas. Still, the country imports around 5 million metric tons of urea a year, with roughly 20% historically coming from the now-disrupted Gulf producers. Domestic ramp-ups and shifts toward Russian and other non-Gulf sources help, but urea-specific price spikes and spring demand pressure remain real risks.

Europe is more exposed. High natural gas costs from earlier energy shocks have already hurt local competitiveness. The EU leans heavily on Algeria and Egypt for urea and ammonia imports (routes not directly blocked by Hormuz), but regional gas issues and higher marginal costs have still pushed European urea prices up roughly 40% since the conflict started. Bottom line: neither region can fully dodge the global price transmission in the short run.

How This Hits Fertilizers, Food Prices, and the 2026 Planting Season

Urea prices have already jumped 27–50%+ since late February. Benchmark granular urea moved from the $450–500/ton range to $650–700+ in key markets. Retail prices farmers actually pay have followed suit—U.S. nitrogen products are up 20–47% month-on-month in some segments. Surveys show 48–70% of U.S. farmers (even higher in the South) say they’re struggling to afford full fertilizer loads for 2026 crops. That’s leading to lower application rates, some shifts from corn to soybeans, and squeezed margins.

Northern Hemisphere spring planting is underway right now in May 2026, so timing couldn’t be worse. Lower nitrogen levels directly mean lower yields for corn, wheat, and other staples. The pain is even sharper in import-heavy regions like India (which sources over 40% of its urea from the Gulf) and Brazil. Early signals point to global food price increases of 3–18% by year-end, depending on how long the disruptions last and how fast inventories draw down.

For those following Truflation data, this means clear upside risks to food CPI components, fresh pressure on headline inflation prints, and potential tailwinds for agricultural commodity futures.

Near-Term Availability and What’s Next

Existing inventories and locked-in contracts are giving major producing countries decent coverage for the immediate 2026 planting window. The U.S. and Europe have pulled from stocks, and alternative suppliers (even Russia), and some big importers report enough domestic or contracted volumes for near-term needs. But the “war premium” baked into prices plus logistics bottlenecks (trucking, rail, barges) point to tightening beyond Q2. A drawn-out Hormuz disruption would push the effects deeper into the second half, harvest season, and 2027 planning.

From a macro view, sustained higher input costs threaten farm profitability, possible acreage cuts, and stickier food inflation—variables that matter a lot for central bank policy, bond yields, and equity rotation (favoring certain agri-input or commodity plays while pressuring food processors). Risk assets feel the indirect heat through inflation expectations and USD dynamics.

Bottom line

The urea shock is real, it’s happening now, and it’s feeding directly into higher food inflation risks just as planting season kicks off. We’ll keep a close eye on urea futures, port throughput numbers, and fertilizer price indices for fresh updates.

For institutional clients who want deeper quantitative modeling on food CPI pass-through or hedging angles, our team is here. Real-time, unbiased inflation data and macro analysis remain at the heart of what we do at Truflation. Stay tuned—we’ll be back with more as the situation evolves.